HEALTH RELATED PROPERTY UNDER THE MICROSCOPE

- Since the Covid pandemic emerged, health-related needs from consumers and businesses have become even more a key concern translating themselves into demand for specialized property linked mostly to residential and offices. This in turn has been triggering more interest from private investors in recent year.

- Apart from the short term, secular trends drive health-related consumer spending in Europe, which is estimated to grow by 14% over the next five years. Aging and sufficiently wealthy populations will continue to require more care and products while also being able to afford them.

- As a result, revenues for health-related companies are expected to rebound post Covid, even though pharma has been resilient. With the rising costs of inpatient hospital stays, many services are increasingly diverted to outpatient clinics and senior housing and care homes prompting demand for these specialized property segments.

- Despite currently strong operators diversifying and expanding across Europe (partly through M&A), UK and US experience has shown investors that the credit quality of operators can be harmed by too aggressive expansion and leverage.

- From a risk perspective, investor risk for higher specified or medicalized properties is not necessarily higher than regular residential or offices as the stability of the cash flow might be stronger, especially with a solid credit rated operator.

- Average prime yields for senior housing investments across Europe were reported at 4.3% with other healthcare-related yields at 4.8%. This indicates excess yields of 130 bps for senior housing relative to residential and 110 bps for healthcare relative to offices, respectively. On a risk-adjusted basis, health-related properties offer an attractive opportunity which could benefit from yield spreads tightening as more investors get into the sector.

Average Prime Yields By Sector (%) – Q2 2021

Source: CBRE, Cushman, AEW Research & Strategy

KEY DRIVERS OF HEALTH-RELATED PROPERTY

HEALTH-RELATED SECTORS SPAN ACROSS PROPERTY TYPES

- Since the Covid pandemic emerged, health-related issues have become the main focus of our daily life but have also attracted more investors’ attention.

- Health-related needs from consumers and businesses translate themselves into demand for specialized housing, offices and labs.

- Conceptually, we find it useful to show the main health-related property sub-types based on the dimensions of medical specificity and length of stay.

- Regarding housing, longer stays are prevalent for senior housing as well as care homes, but medical needs are typically higher for care home residents.

- With clinics, there is an even higher medical specification with needs for operating theatres, treatment and patient rooms, while length of stay is short.

- Specialised medical offices require higher levels of plumbing and ventilation than offices with basic health-related tenants, like doctors and dentists.

- Labs and R&D facilites require the highest level of building specification with industrial strength HVAC and high level security and safety systems. As a result, the length of lease is typically long to recoup the high upfront costs.

Health-related Real Estate Sub-Categories

Source: AEW Research & Strategy

AGING POPULATION DRIVES DEMAND FOR HEALTH-RELATED PRODUCTS & SERVICES

- One of the key driver for the increased demand for health-related goods and services is the increasing share of over 65 year old people.

- Even when living in their own homes, seniors have a higher natural need for more medical care and medicines than younger people.

- Apart from the increasing share of older people in overall population, older people also live longer than ever before. This is partly due to more healthy life styles, but also due to advances in medical science.

- In addition, with high levels of home ownership among older people they have the accumulated wealth to afford more and more advanced medical goods and services during the latter phase of their longer lives.

- All of this is good news for pharmaceutical companies, medical goods producers and medical service providers.

- Countries like Italy, Germany, France, Netherlands and Spain will all have 20% or more of population at 65+ age in only five years from today.

Population ages 65 and above (% of total)

Source: Oxford Economics (WDI World Bank, United Nations projections), AEW Research & Strategy

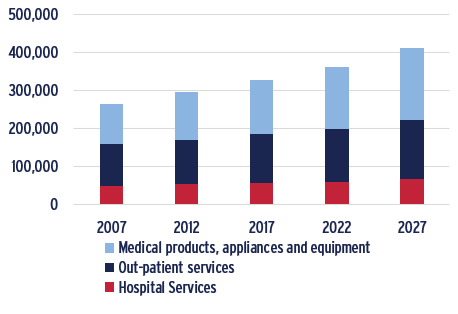

14% GROWTH IN EU HEALTH-RELATED SPENDING BY 2027

- Health-related consumer spending is estimated at a staggering US$ 360 trillion across the EU, with hospital services making up the smallest share.

- Over the next five years, Oxford Economics forecasts a further 14% growth in this spending. This is well above growth for the overall economy.

- Medical products, appliances and equipment is the largest and fastest growing share. Advanced treatments have been facilitated by increasingly advanced technology and new products have driven the costs up.

- This diversified and growing consumer demand base supports the development, manufacturing and use of a very wide range of health-related products and services.

- The expertise needed for these increasingly advance products and services also requires more highly educated staff than ever before.

- In the end, this means that this growing demand supports a high value add industry that has more or less specialised space requirements that it should be able to afford as the need for medical care is as central as life itself.

EU Consumer Spending – Health (US$ MN)

Sources: Oxford Economics, AEW Research & Strategy

GROWTH AND CONSOLIDATION DRIVE HEALTH COVENANT

NON-PHARMA REVENUES PROJECTED TO REBOUND

- While pharmaceuticals benefited, health care equipment and services were hit hard during the lockdowns as patient needs centered around Covid.

- The successful rollout of vaccines is expected to drive revenue up in 2021 as delayed procedures and treatments resume, although staff capacity could remain a bottleneck in the short term.

- Pharmaceutical makers revenues have been helped by record levels of demand for Covid-19 vaccines while increased use of tele-medicine and prescription mail order kept normal prescription volumes high.

- Despite the expected increases in revenues, margin pressure could persist, given overall staff shortages and inflation on salaries for qualified staff.

- Given its crucial role in solving the Covid crisis, the broader health care sector should continue to benefit from government financial support should the pandemic linger late into 2022, albeit at a perhaps reduced level.

Health Care Industry Global Revenue Growth (Local Currency)

Sources: S&P Global Rating Outlook, AEW Research & Strategy

OPERATOR DEMAND FOR OUT-PATIENT & LONG TERM CARE FACILITIES TO GROW

- Healthcare systems are organized and financed in different ways across the EU, which explains the differences in expenditure breakdown in the chart.

- Hospitals are the largest providers of healthcare in expenditure terms, accounting for more than one third (36%) of all expenditure in the EU.

- The hospital expenditure share is highest in Southern Europe while representing less than 28% in Germany.

- We expect other countries reduce their hospital share, like in Germany, as inpatient hospital stays become too costly, many services are diverted to outpatient facilities, which can be funded through sale-lease-backs.

- As a result, operators’ demand for out-patient clinics is expected to grow.

- Long term care is in the other providers category. In the chart. The Netherlands has the highest (28%) expenditure share since it has had a public long-term care insurance system in place since 1968.

- Regardless of public or private funding, the aging population across Europe should drive the operator demand for senior housing and nursing homes.

Healthcare Expenditures on Major Providers, 2018 (% of Current)

Sources: Eurostat, AEW Research & Strategy

KEEP AN EYE ON CREDIT QUALITY OF OPERATORS

- Given that the broader health care sector remains fragmented with increasing margin pressure and significant economies of scale, we expect that merger and acquisition (M&A) activity will resume post Covid.

- Pharmaceutical companies resort to M&A to broaden their drug portfolios while medical device manufacturers and life science companies continue consolidation to diversify their offerings.

- The long-term and medium-term stay sector has also become increasingly consolidated with the largest French long term care groups expanding into other countries, including Germany and Spain and into senior housing.

- Similarly, the medium-term stay and clinics market is dominated by care home operators or short-stay hospital groups which expanded their services in order to optimise continuity of care and manage capacities.

- But as UK and US experience shows it is important to consider that the credit quality of operators can be harmed by too aggressive expansion and financial and operational leverage through sale-lease-backs. A parent company guarantee from a well rated operator can cover this risk. Credit scores might vary across different providers and investors should reconcile between these.

Leading Pan European Long Term Care Operators

Sources: Companies sites, Ellipro, S&P, AEW Research & Strategy

TRENDS IN HEALTH-RELATED PROPERTY MARKET

INVESTORS APPETITE DRIVE UP LIQUIDITY

- Even before the Covid crisis an increase in health-related investment volumes was emerging in 2016-17. This upward trend was further confirmed during 2021, which likely included some catch-up from delayed 2020 deals.

- Dominated by senior housing and care home deals before 2021, health-related deal volumes include predominantly pre-funding deals to finance expanding operators/developers many using the sale-lease-back structure.

- Medical office volumes have remained stable throughout the period has remained stable at close to EUR 1bn pa.

- R&D and lab space volumes across Europe did show a dramatic increase in 2021 to near EUR 4.5bn, more than double the annual volumes recorded in both 2019 and 2020. If the European market follows the US example, this could be expected to continue resulting in a more balanced market.

- The Covid situation might have triggered a lasting interest from investors in R&D and lab space as life science and pharmaceutical firms will need to step up their R&D activities to deal with future crises.

Investment Volumes, Europe (€MN)

Sources: RCA, AEW Research & Strategy

AVERAGE EUROPEAN PRIME YIELDS AT 4.3-4.8%

- Average prime yields for senior housing investments across Europe were reported at 4.3% with other healthcare-related yields were at 4.8%.

- It should be noted that the precise definitions for sub-sectors within the broader health-related segment across our various data providers vary, which is unsurprising for an emerging property type.

- Consistent with other property sectors, German yields are lower than the European average reflecting low bond yields and strong investor demand. In contrast to the rest of Europe, healthcare yields are below senior housing.

- French senior housing yields are at the same level as in Germany, which is likely due to the strong French legal framework for development funding of new facilities and the expansion of French operators.

- On the other hand, the data indicates attractive prime yields of 6% for healthcare properties and near 5% for senior housing in Spain and Netherlands.

Average Prime Yields By Country (%) – Q2 2021

Sources: CBRE, Cushman & Wakefield, AEW Research & Strategy

100+ BPS EXCESS YIELD SPREAD TO CORE SECTORS

- When we compare the prime yields for health-related properties, the data indicates excess yields of 130 bps for senior housing relative to residential and 110 bps for healthcare relative to offices.

- The current excess yields are likely a reflection of the historical niche character of these health-related sub-sectors.

- However, as investor understanding and liquidity improves, it would not be unreasonable to expect lower excess spreads going forward.

- From a risk perspective, investor risk for higher specified or medicalized properties is not necessarily higher than regular residential or offices as the stability of the cash flow might be strong.

- In the case of senior housing, investors are shielded from the risk of individual residents as the lease is with a single professional operator, whose credit risk can be assessed from a corporate perspective.

- In the case of medical offices and R&D or lab space, even smaller tenants are likely to make significant investments in the space themselves incentivizing them to stay longer than normal office tenants to recoup these costs.

Average Prime Yields By Sector (%) – Q2 2021

Sources: CBRE, Cushman, AEW Research & Strategy

This material is intended for information purposes only and does not constitute investment advice or a recommendation. The information and opinions contained in the material have been compiled or arrived at based upon information obtained from sources believed to be reliable, but we do not guarantee its accuracy, completeness or fairness. Opinions expressed reflect prevailing market conditions and are subject to change. Neither this material, nor any of its contents, may be used for any purpose without the consent and knowledge of AEW.